The private markets data problem isn't volume – it's structure

Most private markets firms have more data than they ever wanted:

- Ten-plus years of deal and fund documents scattered across VDRs and drives

- Quarterly financials and KPI packs arriving in different formats every time

- Portfolio monitoring tools, fund accounting systems, and CRMs that all have partial views of reality

The real problem is not volume. It is structure.

LPs, regulators, and internal stakeholders now expect:

- Faster, more granular portfolio insights

- Defensible valuations tied to actual documents and performance

- LP reporting that lines up with ILPA-style templates and regulatory expectations

You cannot get there with scattered spreadsheets and ad hoc exports. You need a portfolio data layer.

Why "just buy a portfolio monitoring tool" isn't enough

Over the last decade, many funds adopted portfolio monitoring and data management tools. They helped, but most were built on an implicit assumption:

Clean, structured data will show up from somewhere.

In private markets that is rarely true.

Reality:

- Portfolio companies send different financial layouts every quarter.

- Key economics and governance terms live in SPAs, LPAs, and side letters, not tables.

- Third-party fund admins and internal teams maintain overlapping but inconsistent datasets.

If you bolt a new UI on top of that, you still have the same underlying problem.

A "portfolio data layer" is about fixing the substrate, not just the dashboard.

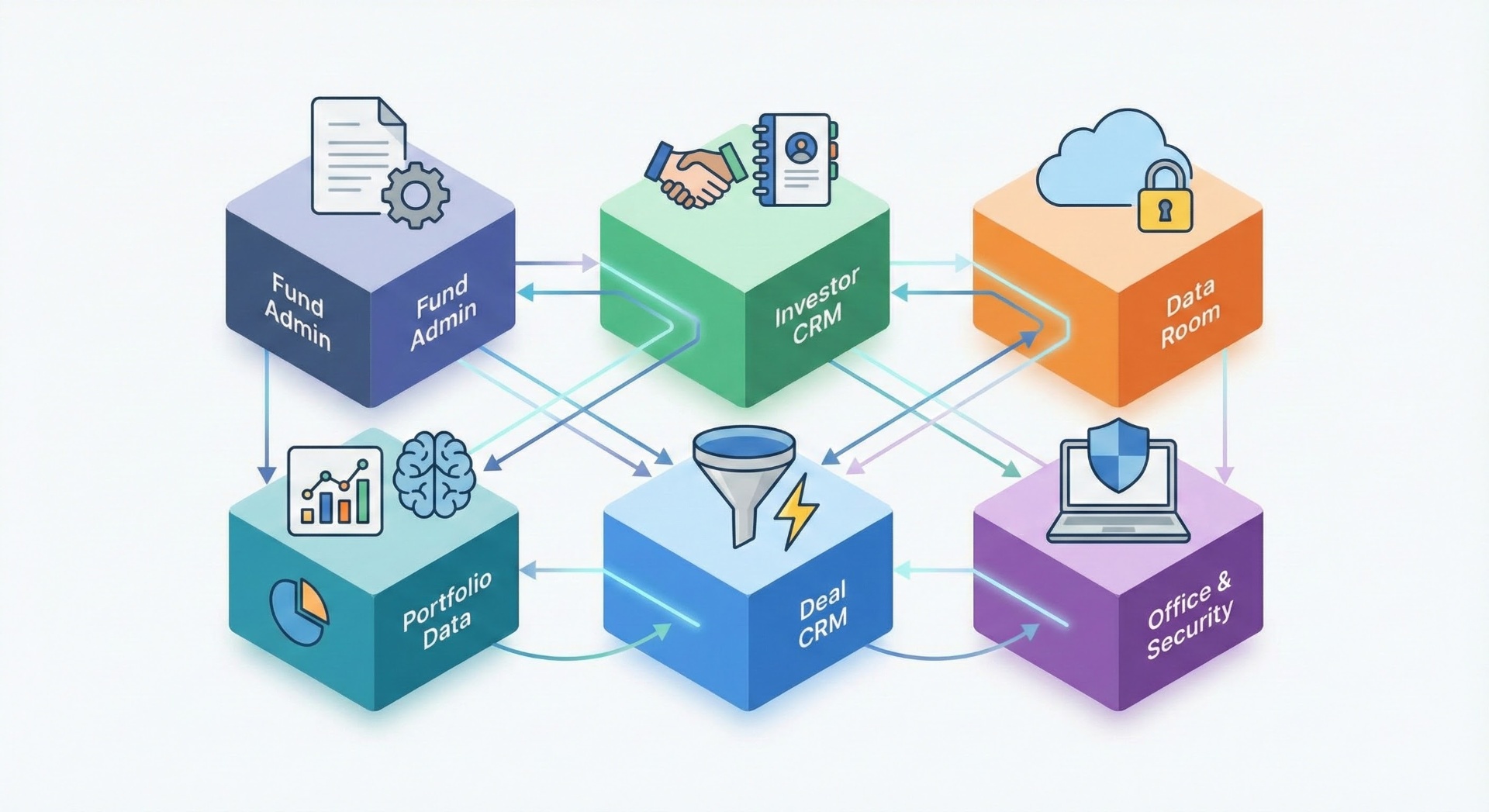

What a portfolio data layer actually is

Think of the data layer as the missing middle between raw inputs and applications:

- Below it are documents, emails, CSVs, data rooms, fund admin exports, and APIs.

- Above it sit valuations, LP reporting, portfolio monitoring, risk analytics, and CRM views.

In practical terms, a portfolio data layer for private markets must:

- Understand entities – funds, legal entities, companies, deals, instruments, investors.

- Be document-aware – every critical data point should be traceable back to specific clauses or rows in specific documents.

- Support multi-asset, multi-fund structures without turning into a ball of spreadsheets.

- Provide clean, governed tables that downstream tools can rely on.

If you cannot say where a number came from or who last changed it, you do not have a data layer. You have a set of shared folders.

Design principles: schema first, documents always in the loop

Before thinking about tools or AI, lock in a few principles.

1. Schema before models

Define, per document type and workflow:

- Which fields you care about (for example, liquidation preference, consent rights, KPI definitions).

- How they should be stored (data types, lookup tables, relationships).

- Which workflows depend on them (valuations, LP reporting, compliance, internal dashboards).

AI extraction without a schema is just a fancy copying machine.

2. Document lineage and auditability

Every key data point should be able to answer:

- Source: which document and section did this come from?

- Version: which version of the document and extraction config produced it?

- Review: has a human validated it, and if so, when?

That lineage is what makes LP and regulatory conversations calm instead of adversarial.

3. Human-in-the-loop, by design

Private markets documents are too bespoke and high-stakes for unsupervised automation.

The data layer should:

- Attach confidence scores to extracted fields.

- Route low-confidence or high-impact fields to human review.

- Capture corrections and feed them back into evaluation and model tuning.

You are building infrastructure, not a one-off experiment.

The four layers of a modern portfolio data stack

A useful way to think about the architecture is as four horizontal layers.

1. Ingestion

- Connect email, data rooms, shared drives, fund admin exports, and APIs.

- Normalize file naming and metadata where possible.

- Deduplicate and version-control documents.

2. Extraction and normalization

- Use AI and rules to classify documents (SPA, note, cap table, LPA, side letter, board deck, financial pack, KPI export).

- For each type, apply the schema you defined and extract fields into structured tables.

- Normalize portfolio company financials into consistent layouts (for example, standard income statement and cash metrics).

3. Data model and governance

- Maintain canonical tables for funds, entities, companies, instruments, investors, and documents.

- Enforce referential integrity and basic business rules.

- Implement role-based access so only the right people can edit sensitive fields.

4. Applications and analytics

Once the first three layers are stable, you can safely plug in:

- Valuation models and memo templates that read directly from the data layer.

- LP and regulatory reporting aligned to ILPA and other standards.

- Internal portfolio dashboards and alerts.

- CRM and fundraising tooling that leverage accurate portfolio data.

Without the lower layers, these applications will always feel brittle.

Build, buy, or "intelligent co-source"?

When funds decide to get serious about their data layer, they usually face three options.

Custom build

- Pros: maximum control, tailored to your strategy.

- Cons: very expensive, hard to maintain, often dependent on a few key engineers or consultants.

Most mid-market managers underestimate the ongoing cost of keeping custom data infrastructure current as documents, regulations, and systems change.

Point tools + consultants

- Data collection tools, portfolio monitoring tools, reporting tools, and BI on top.

- A consulting partner glues everything together and builds custom ETL.

This can work, but often leads to:

- Multiple overlapping data stores.

- Heavy manual work to keep mappings up to date.

- Difficulty adopting new AI capabilities without rewriting flows.

Integrated, AI-first platform (plus targeted services)

Here the data layer, ingestion, and portfolio monitoring live in one platform that:

- Is designed around private markets entities and documents.

- Uses AI for classification and extraction with governance built in.

- Exposes clean, well-documented tables and APIs for other systems.

You still need people and process, but the foundation is no longer bespoke.

A realistic roadmap for a mid-market fund

You do not need to rebuild everything at once. A pragmatic path might look like:

Months 0–6

- Inventory your key documents, systems, and data flows.

- Define schemas for 3–5 critical document types (SPAs, notes, cap tables, LPAs, financial packs).

- Stand up initial ingestion and extraction for those.

Months 6–18

- Expand coverage to amendments, side letters, and more nuanced KPIs.

- Integrate the data layer with fund accounting, CRM, and LP reporting.

- Begin migrating valuations and internal dashboards to rely directly on the new data.

Beyond 18 months

- Introduce more advanced analytics and risk metrics.

- Experiment with agents that watch the data layer for anomalies and events.

- Retire legacy shadow systems as trust in the new layer grows.

The biggest anti-pattern is trying to "do AI" before you know what you want the data to look like.

What "good" looks like in two to three years

When the portfolio data layer is real, you can answer questions like:

- "Show me every company with participating preferred above 1x and revenue below plan for two quarters."

- "Which LPs have reporting obligations that differ from our standard LPA language?"

- "How many days did it take us to respond to the last five LP data requests, and what did they ask?"

You will not get there by plugging another spreadsheet into another dashboard.

You get there by treating your documents and portfolio data as an asset worth architecting.

Ready to see what a modern portfolio data layer looks like in practice? Book a demo and we will walk you through real implementations.