Why valuations are under a brighter spotlight than ever

Valuations have always mattered. But in the last few years, the level of scrutiny has changed:

- Fundraising is harder and capital is concentrating with managers who can defend their marks.

- LPs are stress-testing reported performance against secondary market pricing and public-market multiples.

- Regulators have made it clear that they expect more transparency around how private fund advisers value assets and present performance, even as some new rules face legal challenges.

At the same time, AI is moving into the valuation process. Deloitte expects that roughly a quarter of private equity firms will be using AI to augment portfolio valuations over the next five to seven years, up from low single-digit adoption in 2023.

The opportunity is obvious: faster, more consistent valuations. The risk is equally obvious: if AI-aided marks are opaque or poorly controlled, they become a liability in LP and regulatory conversations.

What "regulatory scrutiny" actually means in practice

The SEC's 2023 Private Fund Adviser rules - which would have, among other things, mandated quarterly statements with detailed performance and expense disclosures and required fairness or valuation opinions for certain adviser-led secondary transactions - were vacated by the Fifth Circuit in mid-2024.

Even with that ruling:

- The SEC's existing anti-fraud, fiduciary duty, books-and-records, marketing, and custody rules still apply.

- Risk alerts and enforcement actions continue to focus on misleading performance, inconsistent valuation practices, and fee/expense disclosures.

- LPs are using ILPA templates and their own ODD programs to dig deeper into how managers value assets, not just what the reported IRR is.

So the bar is not "follow a specific AI rule." It is "have a valuation process that would stand up in an exam or LP negotiation, even if AI is in the loop."

Where AI can legitimately add value in valuations

Done carefully, AI can help in three main ways.

1. Data collection and normalization

Valuation teams spend a huge amount of time:

- Pulling metrics from portfolio company financials and KPI decks

- Reconciling different layouts and definitions quarter after quarter

- Making sure the numbers in the model match the numbers in board materials and LP reports

AI can:

- Classify and extract key financial and KPI fields from recurring documents.

- Normalize formats (for example, mapping "MRR" vs "subscription revenue" into consistent structures).

- Flag inconsistencies or missing data before a valuation committee sees the pack.

This does not change your valuation judgment. It changes how much energy you spend getting to a clean starting point.

2. Scenario support and sensitivity analysis

AI is strong at:

- Generating and organizing scenarios (for example, downside, base, upside) using parameters you specify.

- Running and summarizing multiple sensitivities on growth, margins, and multiples.

- Comparing a company to peer sets and historical outcomes, as long as you define those datasets.

The human still decides which scenarios are credible and how much weight to put on them. AI just makes it cheaper and faster to explore the space.

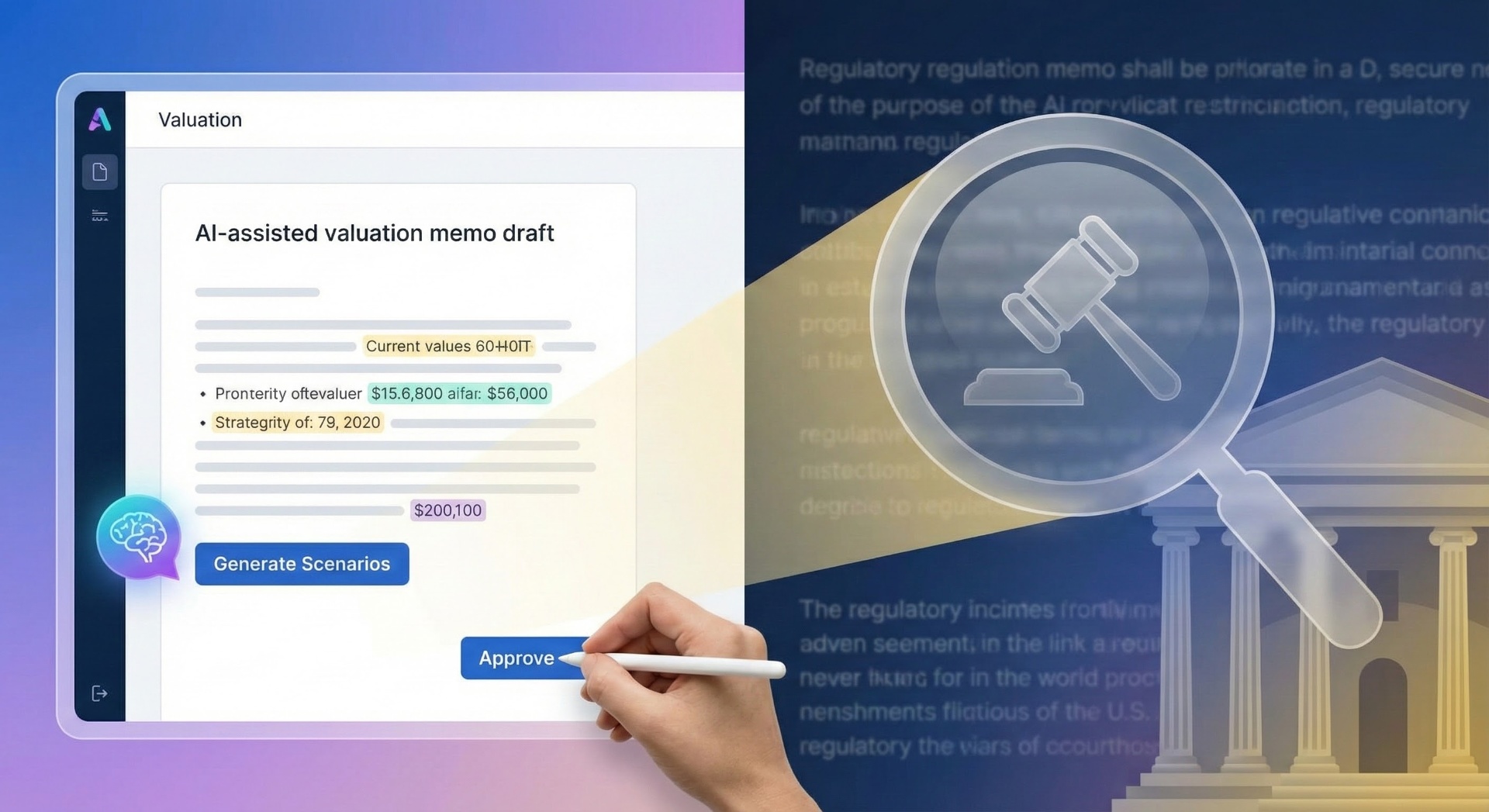

3. Drafting and consistency checks for valuation memos

Valuation memos often repeat structure:

- Company overview and performance since last mark

- Methodologies used (DCF, market comps, recent transactions, scenario analysis)

- Key assumptions and rationale for changes

- Risk factors and watch items

AI can draft sections of memos based on structured data and templates, and can:

- Highlight where the narrative is inconsistent with the numbers (for example, calling performance "strong" when growth has slowed).

- Compare language across memos to spot unexplained differences in methodology or tone.

Again, the human signs the memo. AI just accelerates the drafting and QA.

Where AI should not be left alone

There are areas where letting an AI system act without tight controls is asking for trouble:

- Choosing valuation methodology automatically. Whether you use a market-based, income-based, or hybrid approach is a matter of judgment and policy. AI can suggest options; it should not unilaterally decide.

- "Filling in" missing data. Imputing values for missing metrics or cash flows may be useful analytically, but those values should never silently become official marks.

- Optimizing marks for optics. Any process where AI is implicitly encouraged to find a mark that "looks good" rather than one that is defensible is dangerous.

The standard to apply is simple: could we explain this decision to an LP, auditor, or examiner and show the chain of evidence? If not, AI should not be doing it.

Designing an AI-enabled valuation process that passes the smell test

A credible process has five characteristics.

1. Policy first, tools second

- Document a valuation policy that covers methodologies, frequency, governance, and approval.

- Explicitly state where technology, including AI, is used and where it is not.

- Align this policy with LPAs, side letters, and ILPA-style guidance.

Tools should implement policy, not define it.

2. Clear segregation of roles

- Data layer owners are responsible for data quality, document linkage, and extraction pipelines.

- Valuation teams own methodologies, assumptions, and final marks.

- Risk/compliance owns oversight, testing, and escalation pathways.

AI typically lives in the data and drafting layers, not as the sole owner of any step.

3. Versioning and audit trails

For any given mark, you should know:

- Which data set was used, and when it was last refreshed.

- Which AI models and prompts were involved in data prep or memo drafting.

- Who ultimately approved the valuation and when.

Deloitte and others stress that as AI adoption grows, firms need strong governance and monitoring to demonstrate control over AI-enabled processes.

4. Stress testing the system itself

Just as you stress test portfolio companies, you should stress test your valuation system:

- Run historical periods through the AI-enabled process and compare outcomes to prior marks.

- Review where AI suggestions would have pushed marks higher or lower.

- Assess whether those differences would have been caught by your governance process.

If AI erodes conservatism or creates invisible drift, you will see it here.

5. Transparent communication with LPs

LPs are already asking whether and how managers use AI. Industry commentary suggests that LPs prefer managers who can explain their AI usage clearly over those who claim to have no AI at all.

You do not need to give a technical lecture. You do need to be able to say:

- Where AI is used and why.

- What controls and human oversight are in place.

- How you ensure that marks remain fair and consistent across time.

A pragmatic 12–18 month plan

If you are just starting to introduce AI into valuations:

First 3–6 months

- Focus on data collection and normalization for your top 20 holdings.

- Use AI to assist with document ingestion and financial/KPI extraction into a controlled data layer.

- Keep actual valuation calculations and memos manual.

Next 6–12 months

- Introduce AI-assisted scenario analysis and memo drafting for a subset of companies.

- Implement confidence scores and human review for extracted fields.

- Begin documenting the AI-enabled process as part of your valuation policy.

Beyond 12 months

- Expand coverage to more of the portfolio and more workflows (for example, adviser-led secondaries, continuation vehicles, or evergreen structures).

- Periodically back-test the system and update governance as regulations and standards evolve.

The goal is not to have "AI valuations." The goal is to have better valuations – faster, more consistent, and more defensible – with AI in a clearly controlled and explainable role.

Ready to see how AI fits into a defensible valuation process? Book a demo and we will walk you through real examples from funds like yours.